Mercury Focused Funding

Overview

Mercury's deposit rate was plateauing despite a tidal wave of new applications after the Silicon Valley Bank collapse. I redesigned the focused-funding flow with deliberate friction, and lifted Day 30 deposits by 7%. That added ~$2.3M ARR 🎉.

My role

Lead Growth Designer,

Activation

The team

1 x Growth PM (interim)

1 x Growth Engineer

1 x Junior Designer

1 x Data Scientist

7 x Engineers

Timing / Duration

2025 / 2 tests over 6 months

Background

Mercury is a fintech serving startups and SMBs that offers financial-management software on top of a core banking product. In early 2023, the Silicon Valley Bank collapse sent a tidal wave of new applications our way. But the conversion math wasn't keeping up: only ~59% of approved applicants actually deposited. Leadership made a strategic growth bet to capture the high-intent users coming through the door before that wave subsided.

The pre-existing UX was passive and let users wander in with a dashboard module, empty states, and upsells across the product. The bet I was making: that wasn't forceful enough.

The problem

- ~41% of approved applicants never funded their account

- Mercury is functionally useless without a deposit. Every other feature is downstream of having money in the account

- Activation was the highest-intent moment we'd ever have with these users, and we were leaving it to chance

Team goals

The growth team had three concurrent goals: grow deposit rate, deposit quality (amount), and grow invoicing adoption. The focused-funding work touched all three.

My Process

Discovery

I started by interviewing both funded and unfunded approved applicants. The hypothesis I was most worried about: that a forceful funding gate would feel constraining and people would bail.

The interviews flipped that. Funded users didn't even remember the funding moment of their flow. It was just part of opening a bank account. Unfunded users said something similar in concept: of course you'd have to deposit at some point. You're a bank.

Mercury isn't valuable if you don't deposit money into it. Despite all the cool features we offer, none of them matter without funds in the account.

This is the kind of friction growth designers usually avoid. The team agreed it was the one moment in the funnel where a full-stop is justified.

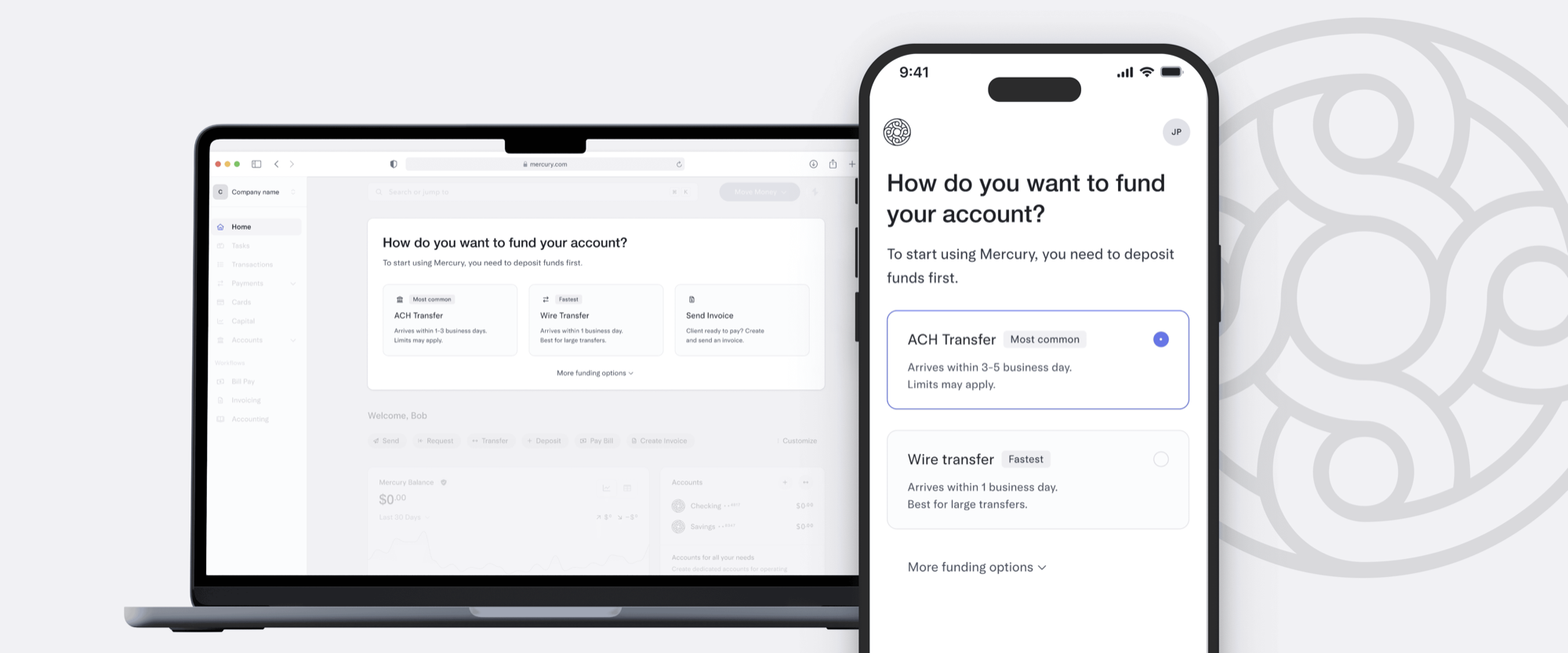

V1: The bet

We couldn't get full political buy-in for a hard gate up front, so we hedged: a small cohort test (20% of users) to read the directional impact. Even at that sample size, v1 lifted deposit rates significantly, enough to greenlight a broader rollout.

Modal: full takeover vs. embedded

We explored a full-screen modal takeover but landed on an embedded modal that teases the dashboard underneath. Even with friction, you want users to remember what they're working toward.

Funding method hierarchy

The earliest iterations showed every funding method at equal weight on a single screen. After testing, I broke the flow into more steps with bigger click targets and one decision per screen. More steps isn't always worse. Conversational flows with one question at a time beat the dense single-screen layout in usability tests.

V2: The refinements

Six months later, three things changed for the next round:

- International wires. A rising share of applicants were international, and they couldn't deposit in v1.

- Mobile optimization. Mobile traffic was growing too. v1 was desktop-first.

- Invoicing as a funding method. Multivariant test introducing invoicing to capture the professional-services cohort opening accounts to receive their first client payment, and to push on the company-wide invoicing-adoption goal.

Side win: the threshold-amount A/B

One idea I wanted in v1 but had to cut for speed: showing suggested deposit thresholds tied to what each amount unlocks. We came back to it as a fast-follow A/B test. Result: +$1,500 to median deposit amount on ACH and wire flows. Defaults are powerful; defaults with a reason are more powerful.

Hard decision: going to bat for international wires

International wires almost got cut from v2: lower usage than ACH/domestic, hidden behind a progressive disclosure, lots of engineering complexity, and we didn't have a PM on the team to do the discovery. I took on the PM responsibilities myself, liaising with the wires & banking team, learning the nuances of cross-border transfers, doing the due diligence. International ended up being the single biggest driver of the v2 7% lift.

My Learnings

Fill the gap

If something's blocking the work and the role isn't staffed, do the role. Taking on PM responsibilities for international wires felt risky at the time. It was the highest-leverage thing I did in this project.

Pre-fill, and give users a reason why

The threshold-amount test wasn't just "here are some numbers." Each suggested amount mapped to a feature it unlocked. Defaults shape behavior. Defaults with rationale shape it more.

More steps isn't always a bad thing

When each step is a clear, conversational question with big click targets, breaking a flow into more steps can raise completion rates. Density isn't speed. Clarity is speed.

De-risk sensitive tests to win the room

Big growth bets are political. When the test you want to run is the kind detractors will push back on (a hard funding gate, in this case), a small-cohort pilot converts skeptics into believers faster than another deck does. The V1 cohort gave us a clean directional read without putting the funnel on the line. Once the numbers came in, the broader rollout sold itself.